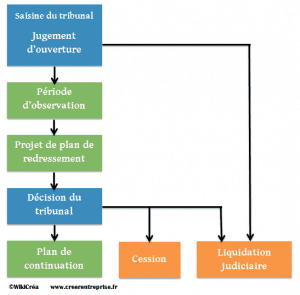

Qu’elles soient individuelles ou qu’elles aient le statut de société, les entreprises faisant face à des difficultés d’ordre financier, et dont le redressement s’avère impossible, doivent solliciter les tribunaux afin de demander l’ouverture d’une procédure de liquidation judiciaire.

Afin de rendre cette procédure plus accessible aux petites entreprises, la liquidation judiciaire simplifiée est désormais ouverte à celles qui ne possèdent pas de bien immobilier, qui n’ont pas employé plus de 5 salariés au cours des six derniers mois et dont le chiffre d’affaires est inférieur à 750 000 euros.

Dans le cas de l’ouverture d’une procédure collective, une question se pose pour les assujettis au RSI: suis-je personnellement redevable des cotisations que je dois à cet organisme ?

Comment se conjuguent liquidation judiciaire simplifiée et RSI et qu’elles sont les formalités à accomplir ?

Le régime social des indépendants (RSI) a été officiellement supprimé le 1er janvier 2018 pour être remplacé par la Sécurité Sociale pour les Indépendants (SSI) qui dépend désormais du régime général de sécurité sociale.

Toutefois, son fonctionnement reste le même et les règles qui lui sont applicables identiques.

Pour l’organisme de Sécurité Sociale des Indépendants, les créances, représentant des cotisations qu’il réclame à ses assujettis, sont considérées comme des dettes professionnelles car elles sont nées de l’activité de l’entrepreneur.

Il considère aussi qu’elles sont dues par l’assuré à titre personnel et non par la société dont il est responsable.

La qualification professionnelle des dettes RSI a été confirmée à plusieurs reprises par des décisions de la Cour d’appel : Cour d’appel de Grenoble du 10 décembre 2013 (RG n°13/01590), Cour d’appel de Caen du 6 février 2014 (RG n°13/01466) et Cour d’appel de Rouen du 20 novembre 2014 (RG n°13/04479, ainsi que par la Cour de Cassation dans un avis n° 16007 du 8 juillet 2016.

S’agissant du sujet liquidation judiciaire simplifiée et RSI, selon le statut juridique choisi par l’assujetti, pour exercer son activité professionnelle, on constate différentes situations :

Liquidation judiciaire simplifiée et RSI, dans certains cas, les cotisations dues à la Sécurité Sociale des Indépendants peuvent être amenées à disparaître en même temps que l’entreprise.

Toutefois, si le RSI considère ces créances comme des dettes personnelles, elles perdurent au delà de la liquidation.

Par ailleurs, au moment de la cessation de l’activité, le RSI peut aussi opérer à des régularisations notamment lorsque le boni de liquidation est pris en compte dans le calcul de l’assiette des cotisations sociales.

Pour éviter un contentieux avec cet organisme, il est prudent de mettre en oeuvre de bonnes pratiques :

Le sujet liquidation judiciaire simplifiée et RSI a suscité beaucoup d’interrogations des entrepreneurs. La jurisprudence sera amenée à apporter des réponses à l’évolution de la réglementation en cours.

PHENIX EXPERTISE est un cabinet de conseil qui accompagne les dirigeants de TPE, PME/PMI, les artisans, les commerçants rencontrant des difficultés financières et qui envisagent la cessation des paiements et une procédure collective (mandat ad’hoc, sauvegarde, redressement ou liquidation judiciaire).

Nous intervenons également dans les cessions et acquisitions de tous types d’entreprise.

Notre cabinet accompagne aussi toutes les personnes porteuses d’un projet de création d’entreprise.